COVID-19: Current and Future Federal Preparedness Requires Fixes to Improve Health Data and Address Improper Payments

Fast Facts

Although hospitalizations and deaths associated with COVID-19 have recently decreased, the pandemic continues to challenge U.S. response and recovery efforts. The federal response continues to focus on vaccinations, testing, and treatment.

As of March 2022, we have made 279 recommendations to improve the federal response, such as collecting data on long-term COVID-19 effects. Agencies have fully or partially addressed 39% of our recommendations.

In this report, we make a suggestion for Congress to consider and 15 new recommendations to address payment oversight, data collection, critical manufacturing and supply chain issues, and more.

Highlights

What GAO Found

By late March 2022, daily COVID-19 cases in the U.S. had fallen substantially since the Omicron-related peak in January 2022. Though COVID-19-associated hospitalizations and deaths have also decreased, the effects of the Omicron variant—and the rising prevalence of its new BA.2 sublineage—underscore enduring challenges and the importance of a continued, agile federal response.

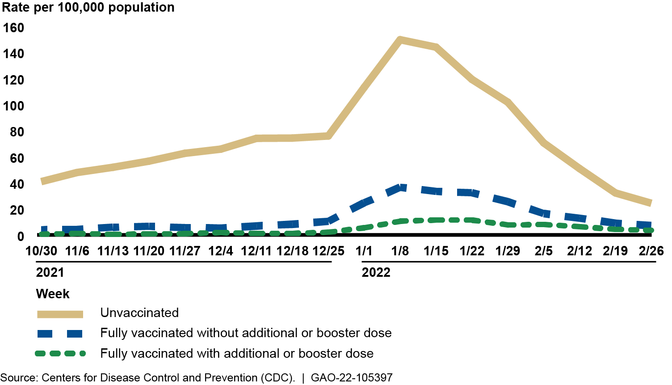

This response has included a focus on COVID-19 vaccinations. As of March 26, 2022, about 70 percent of the eligible U.S. population had been fully vaccinated. According to the Centers for Disease Control and Prevention (CDC), getting vaccinated and staying up to date with vaccines—including a booster dose—is the best way to protect against COVID-19. Data show that vaccinated adults experienced lower COVID-19-associated hospitalization rates (see figure).

Age-Adjusted Rates of COVID-19-Associated Hospitalizations by Vaccination Status in Adults Aged 18 Years and Older, Oct. 2021–Feb. 2022

Since June 2020, GAO has made 279 total recommendations for improving federal pandemic operations. These recommendations include improvements in such areas as publicly reporting COVID-19 nursing home vaccination data and targeting vaccine outreach to veterans. Agencies have fully or partially addressed 39 percent of these recommendations as of March 2022, fully addressing 22 percent (61 recommendations) and partially addressing another 17 percent (48 recommendations). Fully addressing GAO’s recommendations will enhance federal COVID-19 pandemic response and recovery efforts, and help prepare for future public health emergencies.

In this report, GAO makes 15 new recommendations and raises one matter for congressional consideration in the areas of COVID-19 payment oversight, public health data collection, and critical manufacturing, among others.

Payment Integrity: COVID-19 Spending

The Payment Integrity Information Act of 2019 defines improper payments as any payment that should not have been made or that was made in an incorrect amount (including overpayments and underpayments) under statutory, contractual, administrative, or other legally applicable requirements. Improper payments are a pervasive and growing problem in regular programs across the federal government. They also have been a significant concern in pandemic spending, especially among the largest programs such as unemployment insurance.

Under guidance from the Office of Management and Budget (OMB), agencies are to complete a risk assessment to determine a new program’s susceptibility to significant improper payments after the first 12 months of program operations and, if susceptible, develop corrective actions and report on improper payments the following fiscal year. This means that improper payment information for new COVID-19 programs may not be reported until November 2022. By that time, agencies may have disbursed most or even all COVID-19 funds before assessing risk or developing corrective actions to address potential improper payment issues.

GAO therefore suggested in its November 2020 report that Congress consider in any future legislation appropriating COVID-19 relief funds designating all executive agency programs and activities making more than $100 million in payments from COVID-19 relief funds as “susceptible to significant improper payment.”

GAO continues to believe that expeditiously estimating and reporting improper payments and developing corrective actions to reduce such payments is critical to agency accountability, particularly for new programs that receive large outlays in a given year. GAO reiterates the November 2020 matter, as well as a matter GAO made in a March 2022 testimony suggesting that Congress consider amending the Payment Integrity Information Act of 2019 to designate all new executive agency programs—such as those created specifically to respond to the COVID-19 pandemic—making more than $100 million annually in payments as “susceptible to significant improper payments” for their initial years of operation.

GAO also recommends that OMB require agencies to certify the reliability of submitted improper payment data. OMB neither agreed nor disagreed with this recommendation.

FEMA’s COVID-19 Funeral Assistance and Public Assistance Program

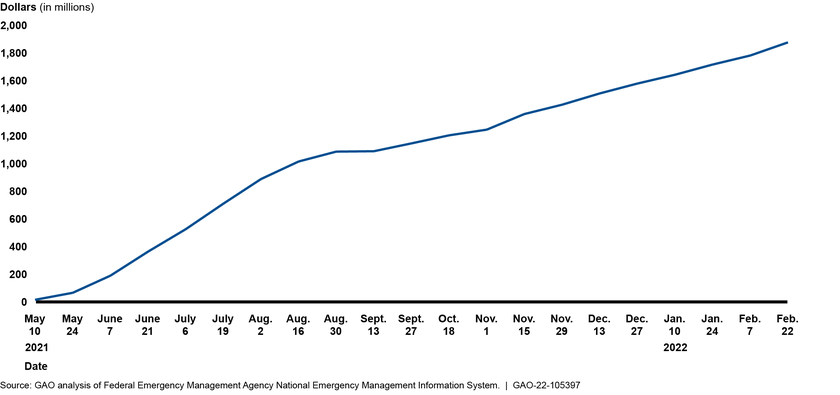

As of February 28, 2022, the Federal Emergency Management Agency (FEMA) had received and was processing more than 444,000 applications for funeral assistance since April 2021—when it began accepting applications—and awarded more than $1.92 billion for more than 296,000 approved applications. (See figure for obligations made for COVID-19 Funeral Assistance from May 10, 2021, through February 22, 2022.)

Cumulative Obligations for FEMA Funeral Assistance over Time, May 10, 2021–Feb. 22, 2022

However, GAO identified several gaps in FEMA’s internal controls meant to prevent improper or potentially fraudulent payments, such as cases in which these controls did not prevent duplicate applications for funeral assistance or assistance issued to ineligible recipients. For example, GAO identified 374 deceased individuals that were listed on more than one award-receiving application; in total, these applications received about $4.8 million in assistance. Without adequate controls in place, COVID-19 Funeral Assistance is at risk of improper payments and potential fraud.

GAO recommends that the FEMA Administrator take action to identify the causes of the gaps in internal control in COVID-19 Funeral Assistance and design and implement additional control activities, where needed, to prevent and detect improper payments and potential fraud.

GAO recommends that the FEMA Administrator address deficiencies in the COVID-19 Funeral Assistance data by updating data records as data are verified, and adding data fields where necessary, to ensure that consistent and accurate data are available for monitoring of potential fraud trends and identifying control deficiencies. The Department of Homeland Security (DHS) agreed with both recommendations.

COVID-19 Surveillance

CDC could be better positioned to lead and coordinate the national efforts to detect and monitor COVID-19 by including in the agency’s existing surveillance approach specific objectives for how it will achieve its goals and a description of how it will assess progress toward meeting them.

CDC’s COVID-19 surveillance approach outlines goals and activities for what the agency wants to achieve, but it does not detail how it will achieve its stated goals or how it will measure its progress—two components of an effective strategy GAO has noted in its past work. By including specific objectives that detail how CDC’s actions will allow it to meet its goals and describing measures to assess its progress towards reaching its goals, CDC could better ensure it is able to effectively monitor COVID-19 nationwide.

GAO recommends that the Director of CDC, in coordination with state, tribal, local, and territorial jurisdictions and public health partner organizations, ensure the agency builds upon its existing COVID-19 surveillance approach by detailing specific objectives for how it will achieve its COVID-19 surveillance goals and describing how it will assess progress toward meeting them. HHS agreed with our recommendation.

Public Health Data Collection and Standardization

CDC has made progress in modernizing the U.S. public health data collection and surveillance infrastructure through its Data Modernization Initiative, which aims to improve data collection and sharing, strengthen data reporting and analytics, and advance surveillance of future public health threats, among other goals.

However, CDC’s strategic implementation plan for the Data Modernization Initiative does not articulate the specific actions, time frames, and allocation of roles and responsibilities needed to achieve its objectives. In addition, CDC has not fully developed plans for how it will allocate certain funds for data modernization. Without more specific, actionable plans, CDC may not be able to gauge its progress on the initiative or achieve key results in a timely manner. In addition, such lack of progress to implement enhanced surveillance systems could affect the quality and timeliness of data needed to respond to future public health emergencies.

GAO recommends that the Director of CDC define specific action steps and time frames for the agency’s data modernization efforts. HHS agreed with this recommendation.

Critical Manufacturing Sector

The pandemic has impacted the Critical Manufacturing Sector by causing worker shortages, delays in shipments of goods, and increased cybersecurity vulnerability in critical infrastructure systems and assets. The Cybersecurity and Infrastructure Security Agency (CISA)—in its role as the lead federal agency for coordinating security and resilience efforts with the Critical Manufacturing Sector on behalf of DHS—took steps to respond to the pandemic’s impacts in the sector. For example, CISA developed voluntary guidance to help jurisdictions and critical infrastructure owners and operators identify essential work functions and ensure that the workers who performed those functions could continue to access their workplaces when restrictions, such as stay-at-home orders, were in place in their communities.

Members of the Critical Manufacturing Sector have identified a lessons-learned analysis as a high-priority need, and CISA has collected some information on the impact of the pandemic in the sector that could be leveraged in a lessons-learned analysis. However, as of February 2022, CISA had not finalized a plan for developing the analysis.

GAO recommends that the Director of CISA assess and document lessons learned from the COVID-19 pandemic’s impacts on the Critical Manufacturing Sector. DHS agreed with this recommendation and stated it plans to issue a lessons-learned report by December 2022.

Advance Child Tax Credit and Economic Impact Payments

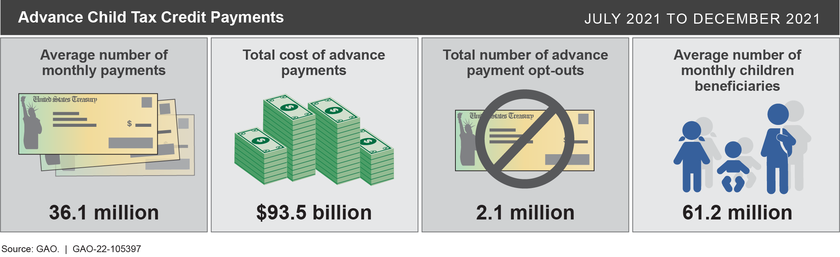

During 2021, the Internal Revenue Service (IRS) and the Department of Treasury issued advance payments of the child tax credit (CTC) and a third round of Economic Impact Payments (EIP 3) to eligible individuals, totaling over $500 billion. Both payments could have had implications for individuals as they filed their 2021 taxes.

Information on Advance Child Tax Credit Payments, July 2021–Dec. 2021, as of April 6, 2022

To help individuals file accurate 2021 tax returns during the 2022 filing season, Treasury and IRS took several steps to reach out to individuals that received the advance CTC payments and EIP 3. However, Treasury and IRS missed opportunities to collaborate on these outreach efforts.

Relatedly, the communications plans and strategies IRS developed for several programs, including the advance CTC and EIP, do not include metrics for assessing the usefulness and accessibility of these outreach efforts. Such metrics would inform management of these efforts and help focus resources on what works. Without sufficient, relevant, timely, and comparable data on its outreach efforts, IRS is missing information it could use to develop performance metrics and to assess which aspects of their communications and outreach strategy were effective in reaching different audiences.

GAO is making three recommendations for Treasury and IRS to enhance communication and outreach efforts concerning the refundable tax credit. These recommendations focus on improving collaboration between the agencies and within IRS and on using data to assess the effectiveness of their efforts. Treasury and IRS neither agreed nor disagreed with the recommendations.

This report contains additional recommendations related to the Single Audit Compliance Supplement, the Capital Projects Fund, the Homeowner Assistance Fund, and Public Health Industrial Base Expansion. For example, GAO recommends that the Assistant Secretary for Preparedness and Response within HHS conduct a workforce assessment of its Innovation and Industrial Base Expansion Program Office to determine the critical skills and competencies needed to support and sustain the office, and develop corresponding workforce strategies to address those needs. HHS agreed with this recommendation.

Why GAO Did This Study

By the end of March 2022, the U.S. had about 80 million reported cases of COVID-19 and over 980,000 reported deaths, according to CDC. The country also experiences lingering economic repercussions related to the pandemic, including rising inflation and ongoing supply chain disruptions.

As of February 28, 2022 (the most recent date for which data were available), the federal government had obligated $4.2 trillion and expended $3.6 trillion for pandemic relief. These amounts reflect 91 and 79 percent, respectively, of the total amount of COVID-19 relief funds provided by the CARES Act and five other relief laws.

The CARES Act includes a provision for GAO to report on its ongoing monitoring and oversight efforts related to the COVID-19 pandemic. This report—GAO’s 10th comprehensive report—examines the federal government’s continued efforts to respond to, and recover from, the COVID-19 pandemic. In addition, GAO’s March 17, 2022 testimony included 10 new legislative suggestions to enhance the transparency and accountability of federal spending, which we reiterate here.

GAO reviewed federal data and documents and interviewed federal and state officials and other stakeholders.

Recommendations

GAO is making 15 new recommendations for agencies and one matter for consideration by Congress that are detailed in this Highlights and in the report.

Matter for Congressional Consideration

| Matter | Status | Comments |

|---|---|---|

| Congress should consider providing the Department of Health and Human Services the authority to require states to report the data necessary for the Secretary to estimate and report on improper payments for the Temporary Assistance for Needy Families program in accordance with 31 U.S.C. § 3352. See the Payment Integrity: COVID-19 Spending enclosure. | No new legislation has been enacted as of March 2024 which would provide the Department of Health and Human Services the authority to require states to report the data necessary for the Secretary to estimate and report on improper payments for the Temporary Assistance for Needy Families program. |

Recommendations for Executive Action

| Agency Affected | Recommendation | Status |

|---|---|---|

| Office of Management and Budget | The Director of the Office of Management and Budget should require agencies to certify the reliability of data submitted to PaymentAccuracy.gov. See the Payment Integrity: COVID-19 Spending enclosure. (Recommendation 1) |

The Office of Management and Budget (OMB) neither agreed nor disagreed with this recommendation. On August 26, 2022, OMB stated that it was planning on adding a new certification requirement for agency submissions to paymentaccuracy.gov, consistent with this GAO recommendation. In September 2022, OMB updated its fiscal year 2022 Payment integrity Annual Data Call Instructions. In this updated document, OMB instructs agencies on how to submit their annual data calls for PaymentAccuracy.gov and directs agencies to certify with their submission that the information provided "is complete and reliable and that the submission has been reviewed and approved by appropriate Agency senior leadership, e.g., the Chief Financial Officer or equivalent." We believe that OMB has addressed our recommendation. Therefore, we are closing this recommendation as implemented.

|

| Federal Emergency Management Agency | The Federal Emergency Management Agency Administrator should take action to identify the causes of the gaps in internal control in COVID-19 Funeral Assistance and design and implement additional control activities, where needed, to prevent and detect improper payments and potential fraud. See FEMA's COVID-19 Funeral Assistance and Public Assistance Program enclosure. (Recommendation 2) |

In April 2023, FEMA officials provided information showing that the agency had taken action to help prevent and detect improper payments and potential fraud. For example, based on our findings, FEMA now manually reviews any applications with pending awards over $9,000 on a daily basis to help avoid improper payments. In addition, FEMA implemented refresher training for staff, to be completed by April 2023, to help clarify how to process potential duplicate applications and verify that assistance does not exceed the maximum allowed. Further, officials reported that in October 2022 FEMA established a new payment integrity and fraud prevention section tasked with review and analysis of potentially fraudulent funeral assistance cases. Officials also reported that as of April 2023 FEMA was performing an audit of a random sample of awarded funeral assistance applications from 2021 and 2022, intended to assess the implementation of FEMA's fraud prevention and other controls. FEMA expects to complete the audit by the end of September 2023.

|

| Federal Emergency Management Agency | The Federal Emergency Management Agency Administrator should address deficiencies in the COVID-19 Funeral Assistance data by updating data records as data are verified, and adding data fields where necessary, to ensure that consistent and accurate data are available for monitoring of potential fraud trends and identifying control deficiencies. See FEMA's COVID-19 Funeral Assistance and Public Assistance Program enclosure. (Recommendation 3) |

FEMA agreed with our recommendation and has taken steps to address it. Officials reported that in September 2023, FEMA updated three staff guidance documents to remind staff to update application data if there are corrections to information such as Social Security Numbers or death dates. Officials also reported that as of October 2022, FEMA had established a new payment integrity and fraud prevention section tasked with review and analysis of potentially fraudulent funeral assistance cases. In addition, in September 2023, FEMA completed an audit of a random sample of applications, finding errors in around 27 percent of 544 applications from calendar years 2021 and 2022. FEMA reported considering updates to guidance in response to recommendations from the audit. While intended to assess FEMA's controls more broadly, these efforts could help identify inconsistent data elements and lead to improvements. However, as of April 2024, FEMA did not have plans to change how data on whether applications were paid, and the amount of funeral assistance awarded for specific decedents on an application with multiple decedents, are recorded. FEMA officials stated that the data are of sufficient quality such that no further action is needed, particularly given the resources that would be required to change the data system of record. We believe that the agency should perform a formal fraud risk assessment to determine risk tolerance and a cost estimate of the resources required to make the necessary changes to justify these claims. Absent those assessments, we continue to believe that the agency should make targeted efforts-such as updates to how data are entered in the system of record-to improve the consistency and accuracy of the COVID-19 funeral assistance data to facilitate oversight and prevent and detect fraud, particularly given that FEMA officials reported the program will extend through September 30, 2025.

|

| Department of Education | The Secretary of Education should document policies and procedures for providing information to the Office of Management and Budget to better enable it to annually update the Compliance Supplement that include steps for (1) establishing management's expectations of staff competence for key roles (e.g., relevant knowledge, skills and abilities) and providing ongoing training, and (2) agency officials proactively involving internal stakeholders (e.g., the inspector general, general counsel and chief financial officer) and external stakeholders (e.g., the audit community) when developing audit procedures, prior to submitting drafts to the Office of Management and Budget, in order to ensure the guidance meets users' needs. See the Single Audit Compliance Supplement enclosure. (Recommendation 4) |

In March 2024, Education informed us that they are in the process of taking action in response to our recommendation and that the estimated completion date for such is June 30, 2024. Specifically, Education officials stated that "the Grants Risk Management Services Division (GRMSD) will take the lead in working with the various program offices to update and/or document policies and procedures for providing information to OMB to better enable OMB to annually update the Compliance Supplement in a manner that meets the needs of its users. GRMSD will work with program offices to review and enhance, where necessary, its current methodology for training and establishing management expectations of staff competencies for key Compliance Supplement roles at the program office level. GRMSD will enhance its policies and procedures to examine and improve its current engagement with internal (e.g., general counsel and chief financial officer) and external (e.g., inspector general and the audit community) stakeholders and where necessary, enhance its policies and procedures to ensure consistency and efficient collaboration is maximized during the Supplement review process."We will continue to monitor Education's steps to address this recommendation.

|

| Department of Health and Human Services | The Secretary of Health and Human Services should document policies and procedures for providing information to the Office of Management and Budget to better enable it to annually update the Compliance Supplement, that include steps for (1) establishing management's expectations of staff competence for key roles (e.g., relevant knowledge, skills and abilities) and providing ongoing training, and (2) agency officials proactively involving internal stakeholders (e.g., the inspector general, general counsel and chief financial officer) and external stakeholders (e.g., the audit community) when developing audit procedures, prior to submitting drafts to the Office of Management and Budget, in order to ensure the guidance meets users' needs. See the Single Audit Compliance Supplement enclosure. (Recommendation 5) |

In February 2024, officials from HHS Office of Grants provided us with their response to the recommendation along with the finalized HHS Compliance Supplement Standard Operating Procedure (SOP).In its SOP, HHS included steps for (1) establishing management's expectations of staff competence for key roles and (2) agency officials proactively involving internal stakeholders (e.g., the inspector general, general counsel and chief financial officer) and external stakeholders (e.g., the audit community) when updating the Compliance Supplement. The SOP states that HHS provides awarding agencies with technical assistance and training. In addition, in April 2024 HHS provided additional information on the types of trainings provided. HHS officials stated: (1) New HHS awarding agency coordinators are trained by the HHS Core Team Member as needed. HHS awarding agency coordinators (new and existing staff) are provided a copy of the current SOP annually; (2) OMB conducts annual training for HHS employees, including the HHS Core Team Member and the HHS awarding agency coordinators at the Compliance Supplement Kick-Off Meeting; and (3) To ensure that the team is keep current with the latest regulations, the HHS Core Team provides individual refreshers to HHS awarding agency coordinators as needed. We believe that HHS's actions and SOP demonstrates that HHS has designed policies and procedures that address the recommendation. Therefore, we consider this recommendation to be closed-implemented.

|

| Department of the Treasury | The Secretary of the Treasury should document policies and procedures for providing information to the Office of Management and Budget to better enable it to annually update the Compliance Supplement, that include steps for (1) establishing management's expectations of staff competence for key roles (e.g., relevant knowledge, skills and abilities) and providing ongoing training, and (2) agency officials proactively involving internal stakeholders (e.g., the inspector general, general counsel and chief financial officer) and external stakeholders (e.g., the audit community) when developing audit procedures, prior to submitting drafts to the Office of Management and Budget, in order to ensure the guidance meets users' needs. See the Single Audit Compliance Supplement enclosure. (Recommendation 6) |

To address this recommendation, Treasury provided its Federal Financial Assistance Award Policy and related Guide. While the documents addressed part of our recommendation, we had further questions about ongoing training efforts for staff who are responsible for providing updates to the Compliance Supplement and sent follow-up emails to obtain additional information. As of April 16, 2024, Treasury has not replied to our follow up questions. We will continue to monitor Treasury's steps to address this recommendation.

|

| Department of the Treasury | The Secretary of the Treasury should document a comprehensive plan that includes timely and sufficient policies and procedures for monitoring recipients of the CPF to provide assurance that funds are being used in compliance with laws, regulations, agency guidance, and award terms and conditions, including ensuring that funds are being used for allowable purposes. See the Capital Projects Fund enclosure . (Recommendation 7) |

The Department of the Treasury (Treasury) agreed with the recommendation. As of April 2024, Treasury had renamed its Office of Recovery Programs (ORP) to Office of Capital Access (OCA) and had taken steps to address this recommendation by issuing several documents detailing internal controls over monitoring recipients of Coronavirus Capital Projects Fund (CPF) awards, including Treasury's latest revision in April 2024 to its Awards Management Policy. Treasury also issued Compliance Testing Procedures for its programs including CPF. Prior to these actions, Treasury had finalized and issued various compliance and recipient monitoring documents responsive to the recommendation. For example, Treasury issued CPF business rules and implemented testing on CPF reports. The first reports for CPF were due in October 2022 and covered all CPF expenditures made by the recipient up until September 2022. Business rules were developed and used to test these reports. In January 2023, Treasury issued its "Single Audit Responsibility Policy" and "Standard Remedies: Non-Submission of Required Compliance Reports and Failure to Register or Lapse of Registration at SAM.gov", and finalized updated policies and procedures for award management and compliance testing that apply to all programs administered by Treasury's OCA, including CPF. In April 2023, Treasury further updated its Compliance Testing Procedures to reflect the business rules that Treasury's recipient monitoring utilizes in its CPF testing process. In June 2023, Treasury published its Compliance and Reporting Guidance for Tribal governments and a user guide. In March 2024, Treasury issued its latest CPF Project and Expenditure Report User Guide for State to help CPF recipients fulfill their quarterly reporting requirements. In March 2024, Treasury issued an updated version of the CPF Compliance and Reporting Guidance for States, Territories, and Freely Associated States. We believe Treasury has addressed our recommendation by completing documentation of its procedures for CPF recipient monitoring to help ensure that recipients are maintaining effective controls over the funds and that funds are expended in accordance with federal requirements.

|

| Department of the Treasury | The Secretary of the Treasury should develop and implement written procedures to monitor Homeowner Assistance Fund participants' programs and uses of funds for compliance with program requirements and improper payments. See the Homeowner Assistance Fund enclosure. (Recommendation 8) |

In April 2023, Treasury finalized data validation, compliance testing, and noncompliance remediation procedures that apply to all programs within the Office of Capital Access-formerly the Office of Recovery Programs-including the Homeowner Assistance Fund. The procedures include monitoring steps specific to the fund that Treasury officials told us in April 2024 are being used to test participants' quarterly and annual financial and performance reports for compliance with program requirements. For example, the procedures include steps to test whether participants' programs indicate compliance with documentation and income eligibility requirements. In addition, Treasury has published a single audit compliance supplement since 2022 to assist local auditors in evaluating participants' programs for compliance with program requirements and has implemented a tracking dashboard to monitor and remediate single audit findings.

|

| Centers for Disease Control and Prevention | The Director of the Centers for Disease Control and Prevention should define specific action steps and time frames for the agency's data modernization efforts. See the Public Health Data Collection and Standardization enclosure. (Recommendation 9) |

In April 2022, we recommended that the Centers for Disease Control and Prevention (CDC) define specific action steps and time frames for the agency's data modernization efforts. In 2023, CDC launched a Public Health Data Strategy under the new Office of Public Health Data, Surveillance, and Technology which defined specific action steps and time frames. In its 2024-2025 Public Health Data Strategy (Strategy), publicly released in April 2024, CDC has further developed the milestones-goals to improve collection and sharing of public health data collection-through 2025. According to the Strategy, as of the end of 2023, CDC had met 12 of 15 milestones for the year. While three milestones remained incomplete, the CDC states it is on track to complete those in 2024. The milestones met in 2023 have helped CDC achieve progress in meeting its broader data modernization goals. For example, CDC met its milestone of receiving and ensuring access to commercial laboratory data from at least two major national commercial laboratories to enable situational awareness across multiple conditions. CDC stated this improved national CDC situational awareness by increasing laboratory data collection across geographies and conditions. In other cases, CDC has surpassed its 2023 milestones. For example, one milestone was having 75 percent of CDC infectious disease laboratories capable of sending laboratory test results to external partners electronically. According to the Strategy, as of April 2024, more than 90 percent of such laboratories send laboratory test results electronically. CDC stated that external partners are now able to quickly receive laboratory test results to enable rapid awareness of public health threats. In light of CDC's Public Health Data Strategy that defines action steps for data modernization and time frames for completion, we are closing the recommendation as implemented.

|

| Centers for Disease Control and Prevention | The Director of the Centers for Disease Control and Prevention, in coordination with state, tribal, local, and territorial jurisdiction and public health organization partners, should ensure the agency builds upon its existing surveillance approach by detailing specific objectives for how it will achieve its COVID-19 surveillance goals and describing how it will assess progress toward meeting them. See the COVID-19 Surveillance enclosure. (Recommendation 10) |

CDC agreed with the recommendation and has taken steps, in coordination with state, tribal, local, and territorial jurisdiction and public health organization partners, to ensure the agency builds upon its existing surveillance approach by detailing specific objectives for how it will achieve its COVID-19 surveillance goals and describing how it will assess progress toward meeting them. For example, in its written response received in February 2024, CDC noted that it coordinated with jurisdictional and public health organization partners by participating in or sponsoring meetings and briefings for pre-decisional information sharing and responsiveness to questions regarding changes to national COVID-19 surveillance indicators with the expiration of the Public Health Emergency declaration in May 2023. CDC published two reports in May 2023 that described the COVID-19 surveillance framework, indicators, and data sources for achieving its surveillance goals and objectives following the expiration of the emergency declaration. One of these articles indicated that the primary goal of national COVID-19 surveillance is to monitor trends in severe COVID-19 (i.e., hospitalizations and deaths). Severe COVID-19 has the greatest public health significance, particularly because highly effective vaccines are available for prevention. CDC described its assessment of a hospital admissions data indicator to meet its goal of monitoring trends in severe COVID-19. Specifically, before the end of the public health emergency, CDC assessed how often hospital admission levels were aligned with the COVID-19 community level data and found good alignment. This suggested that hospital admission levels can be a reliable way to track COVID-19 activity. In written responses received in April 2024, CDC noted that the surveillance data streams have either remained intact or have been successfully adapted to continue to meet its goals and objectives for monitoring trends in COVID-19-associated illness and severe disease. These actions fulfill the intent of the recommendation.

|

| Cybersecurity and Infrastructure Security Agency | The Director of the Cybersecurity and Infrastructure Security Agency should assess and document lessons learned from the COVID-19 pandemic's impacts on the Critical Manufacturing Sector. See the Critical Manufacturing Sector enclosure. (Recommendation 11) |

CISA agreed with GAO's recommendation and, in September 2022, shared with us the Critical Manufacturing Pandemic Planning Guide (published July 2022), which provides suggested guidelines and best practices for Sector members to follow during a pandemic or other similar crisis. CISA's Guide is a positive step in providing the Sector with guidance and best practices for navigating a pandemic or similar crisis, but the Guide does not document the lessons CISA learned from assessing the COVID-19 pandemic's impacts on the Sector. To address this issue, in April 2024, CISA officials provided us with their draft COVID-19 after-action report,. To fully address this recommendation, CISA officials should assess and document, either as part of the Guide or separately, lessons learned from the pandemic's impacts on the Critical Manufacturing Sector. This would help show how the Guide's best practices, or separately identified lessons learned, could mitigate the effects of similar, future crises. We will review the after-action report to see whether CISA has taken steps to fully address this recommendation.

|

| Office of the Assistant Secretary for Preparedness and Response | The Assistant Secretary for Preparedness and Response within the Department of Health and Human Services should conduct a workforce assessment of its Innovation and Industrial Base Expansion Program Office to determine the critical skills and competencies needed to support and sustain the office, and develop corresponding workforce strategies to address those needs. See the Public Health Industrial Base Expansion enclosure. (Recommendation 12) |

The Administration for Strategic Preparedness and Response (ASPR) agreed with GAO's recommendation. In October 2023, ASPR provided information on efforts taken to address the recommendation. Specifically, ASPR provided an assessment of the workforce needs of its new Office of Industrial Base Management and Supply Chain (formerly known as the Innovation and Industrial Base Expansion Office). The assessment included detailed information on the critical skills and competencies needed to support and sustain the office, such as information on the number and types of permanent positions needed, and those that would need to be hired. The assessment determined that 38 additional staff are needed. Of these 38, ASPR plans to covert 10 existing staff currently working for the agency under term positions to permanent positions and plans to hire the remaining 28 staff. In January 2024, ASPR provided general information on the recruiting and hiring strategies they are employing to hire the 28 staff. ASPR's assessment of its workforce needs for this Office are a positive step forward and partially address our recommendation. However, GAO is keeping this recommendation open until we obtain further information on the recruiting and hiring strategies ASPR is employing to hire the additional 28 staff, including actions ASPR is taking to monitor the effectiveness of these strategies.

|

| Department of the Treasury | The Secretary of the Treasury, in coordination with the Commissioner of Internal Revenue, should enhance collaboration among departmental components for refundable tax credit communication and outreach efforts by including relevant participants and clearly defining participant outcomes, roles, and responsibilities. See the Advance Child Tax Credit and Economic Impact Payments enclosure. (Recommendation 13) |

In March 2024, Treasury officials responded that the Department does not have any updates to this recommendation.

|

| Internal Revenue Service | The Commissioner of Internal Revenue should enhance internal collaboration among its stakeholder outreach and education offices for refundable tax credit communications and outreach efforts by clearly establishing outcomes, roles and responsibilities, and developing resources to facilitate joint interactions and methods to document information sharing. See the Advance Child Tax Credit and Economic Impact Payments enclosure. (Recommendation 14) |

The information IRS provided us in 2023 and 2024 focused on Puerto Rico outreach, the EITC, and advance child tax credit during the 2023 filing season. While we continue to identify this recommendation as "open-partially addressed" IRS has not fully closed the recommendation. For example, IRS has not provided us documentation on how internal offices developed (1) outcomes, roles and responsibilities and (2) resources to facilitate joint interactions and methods to document information sharing for all existing refundable tax credits including including EITC, American Opportunity Tax Credit (AOTC), Additional Child Tax Credit (ACTC), and Premium Tax Credit (PTC).

|

| Internal Revenue Service | The Commissioner of Internal Revenue should collect sufficient, relevant, and comparable data on the usefulness and accessibility of its communications and outreach efforts for refundable tax credits and use these data to develop performance metrics to assess the effectiveness of ongoing efforts. See the Advance Child Tax Credit and Economic Impact Payments enclosure. (Recommendation 15) |

In March 2024, IRS officials responded it was unable to provide an update. However, the responsible team is planning to establish milestones in 2026.

|